Financial Reporting Fraud? When Practice Doesn’t Meet Standards: A Look into Nepalese Corporate Financial Reporting !!

Understanding the financial reporting practices of corporations is critical, especially for listed companies where public investors are involved. Unfortunately, some practices in Nepal have been found not to align with standard financial reporting practices. Shivam Cement Limited, a listed company on the Nepal Stock Exchange, serves as an illustrative example.

In the first quarter of the fiscal year 2079/80, an item was included in the ‘Other Income’ section of Shivam Cement Limited’s financials, amounting to over 30 Crore NPR. The initial assumption made by many was that this was a cash dividend received from Hongshi Cement through Shivam Holdings Limited. However, a more in-depth analysis reveals a different story.

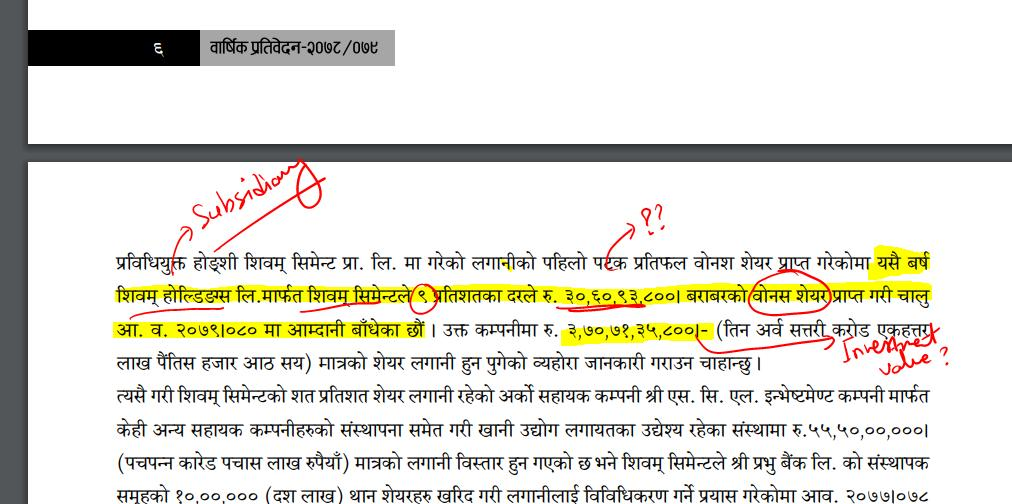

The reported income is not a cash dividend from Shivam Holdings Limited. Instead, it’s the value of bonus shares received from the subsidiary. The company seems to have multiplied the number of bonus shares by 100 and reported it as income in the Profit & Loss statement. This accounting treatment makes it appear as though the company’s investment in its subsidiary has increased to 3.7 Arba NPR. (As per management statement in recent annual report)

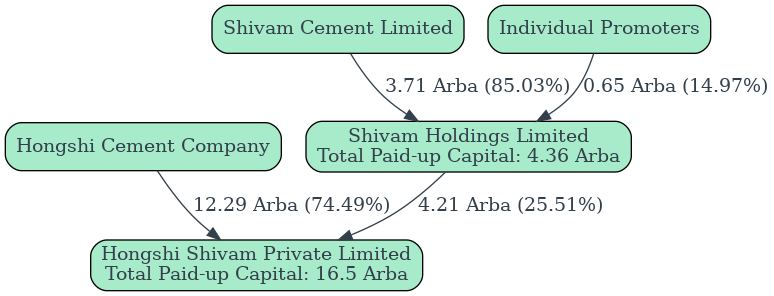

Before proceeding, it’s crucial to understand the capital structure of the involved companies. Below attached is the image of the capital structure.

- Shivam Cement Limited owns an 85.03% stake in Shivam Holdings Limited

- Shivam Holdings Limited then holds a 25.51% stake in Hongshi Shivam Private Limited, representing a share capital investment of 4.21 Arba NPR.

Dividends received from subsidiaries can be in the form of cash dividends or bonus shares. These two forms of dividends are treated differently in financial reporting: Cash Dividends: Cash dividends are treated as income because they represent a distribution of the company’s profits to its shareholders. They should be recorded in the Profit & Loss statement of the parent company. Bonus Shares: Contrary to cash dividends, bonus shares represent a reallocation of the company’s retained earnings. They are not considered income, and instead, they should be recorded as an increase in the number of shares, and by decreasing the cost of shares in the balance sheet of the parent company.

In this case, Shivam Cement Limited seems to have treated bonus shares as income, which goes against standard financial reporting standards.

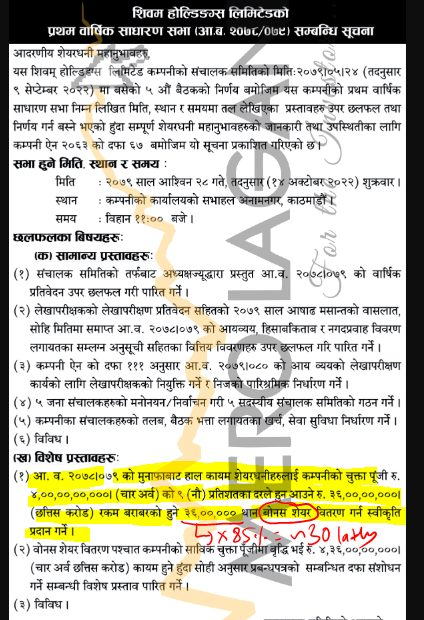

Furthermore, the company has been less than transparent in its disclosures. While the quarterly report mentioned receiving dividends from Hongshi Holdings, it did not explicitly state the nature of these dividends. A check on the Annual General Meeting (AGM) agenda of Shivam Holdings Limited showed a proposal to distribute a 9% dividend to shareholders, amounting to about 30 Crore NPR. This figure, along with the chairman’s statement in Shivam Cement’s latest annual report, gives further confirmation that the dividends were indeed in the form of bonus shares. These kinds of practices can create a murky situation for analysts and investors. It emphasizes the need for diligence in examining line items in financial reports.

As responsible investors and analysts, we must keep a keen eye on these practices and advocate for greater transparency and adherence to standard financial reporting practices. It’s not just about ensuring the correctness of annual audited results but also the quarterly reports as these documents guide investor decision-making.

Let’s remember: When it comes to financial reporting, clarity is king.

Correction: 70% ownership of Hongshi in Hongshi Shivam Cement.

Annexures